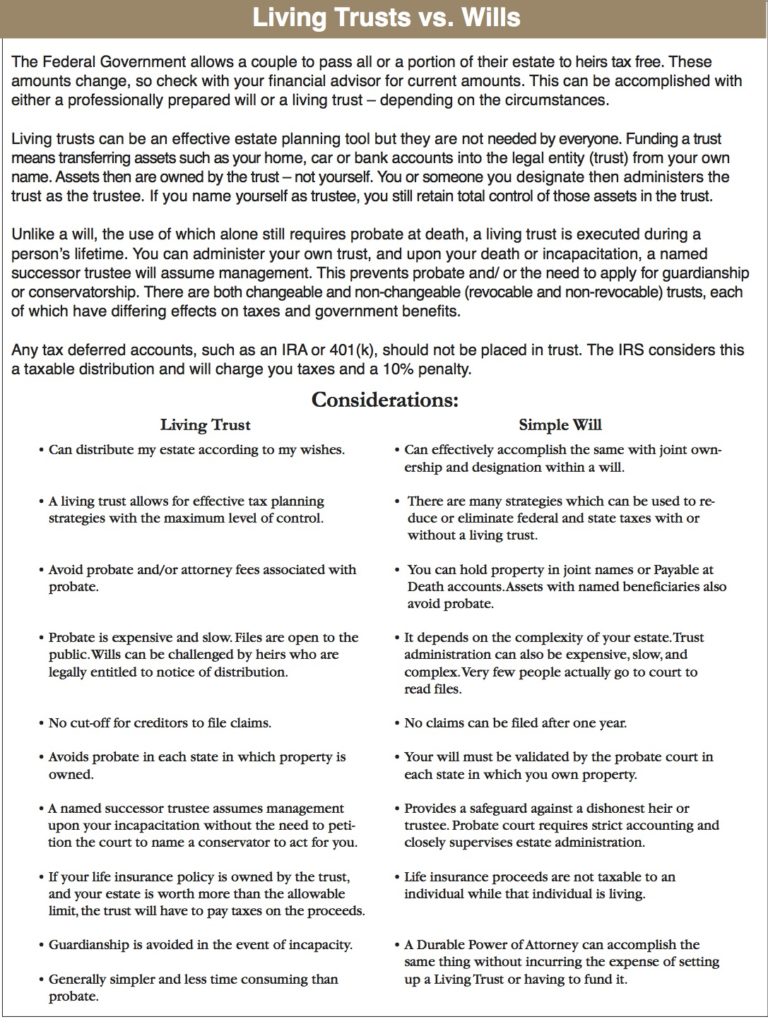

Published on SeniorImpact.com | May 2026 | Cincinnati, Ohio

Medicaid is a lifeline for hundreds of thousands of Ohio seniors, covering everything from nursing home care to in-home assistance to prescription drugs that Medicare alone doesn’t fully handle. But the program evolves every year, and 2026 has brought several changes that seniors and their families should understand. This article breaks down what’s changed, what it means for you, and where to get help navigating the system.

The Medicaid Unwinding Is Still Affecting Ohio Seniors

The COVID-era continuous enrollment protections that prevented states from dropping people from Medicaid ended in 2023, and the effects are still rippling through Ohio’s system. During the “unwinding,” many seniors lost coverage—not because they were ineligible, but because they missed renewal paperwork or because the state had outdated contact information. If you or someone you know was dropped from Medicaid in the past two years, it’s worth reapplying. Eligibility hasn’t necessarily changed; the paperwork process just caught people off guard. Your local County Department of Job and Family Services can help you reapply, and the process can be done online, in person, or by phone.

Income and Asset Limits for 2026

Ohio Medicaid eligibility for seniors is based on income and, in some cases, assets. For the Aged, Blind, and Disabled (ABD) category that most seniors fall under, the income limit is tied to the Federal Poverty Level and adjusted annually. For 2026, a single individual generally qualifies if their monthly income is at or below approximately $1,732 (this figure may have been adjusted—confirm with your caseworker). Married couples have a higher threshold. Asset limits also apply for certain programs, though Ohio has eliminated the asset test for many Medicaid categories. Your home, one vehicle, and certain other assets are typically excluded from the count.

Important: Medicaid eligibility rules are complex and depend on which specific program you’re applying for. The numbers above are general guidelines. Always verify current limits with your County Department of Job and Family Services or a certified Medicaid planner.

Ohio’s PACE Program: A Hidden Gem for Cincinnati Seniors

The Program of All-Inclusive Care for the Elderly, known as PACE, is one of the most comprehensive senior care programs available in Ohio, and many Cincinnati families have never heard of it. PACE is designed for adults age 55 and older who qualify for nursing home-level care but want to remain living at home. The program provides coordinated medical care, adult day services, transportation, meals, home care, prescriptions, and more—all through a single provider. PACE programs are available in most, but not, Ohio counties. Call you local Area Agency on Aging to see if a PACE center serves your ares. If you qualify for both Medicare and Medicaid, PACE can cover virtually all of your healthcare needs with no premiums and minimal or no copays.

The Medicaid Waiver Programs: Staying Home Instead of a Nursing Facility

Ohio operates several Medicaid waiver programs that allow seniors to receive care in their own homes or in community settings rather than in nursing homes. The most relevant for Cincinnati seniors are the PASSPORT waiver and the MyCare Ohio program. PASSPORT provides home-delivered meals, personal care assistance, home modifications, emergency response systems, and adult day care. MyCare Ohio integrates Medicare and Medicaid benefits into a single managed care plan for people who are eligible for both. These programs can make it financially possible to age in place even when you need significant daily assistance. The catch is that waiver programs often have waiting lists, so applying early is important.

What the Federal Medicaid Debate Means for Ohio

At the federal level, there is ongoing debate about restructuring Medicaid funding, including proposals to convert federal Medicaid funding to block grants or per-capita caps. If enacted, these changes could significantly affect Ohio’s Medicaid program and the services available to seniors. While nothing has been finalized as of early 2026, Ohio seniors and their families should be paying attention. Advocacy organizations like AARP Ohio, the Ohio Academy of Senior Health Sciences, and the Universal Health Care Action Network of Ohio are tracking these proposals and can help you stay informed and make your voice heard.

How to Apply or Renew in Ohio

If you need to apply for Ohio Medicaid or renew your coverage, you have several options. You can apply online through the Ohio Benefits Self-Service Portal, call the Hamilton County Department of Job and Family Services directly, or visit their office in person. For help navigating the application, the Council on Aging of Southwestern Ohio offers free Medicaid counseling, and Pro Seniors provides legal assistance for seniors facing Medicaid denials or complications. The Ohio Senior Health Insurance Information Program (OSHIIP) can also help you understand how Medicaid works alongside your Medicare coverage.

Medicaid Planning: It’s Not Too Late

If you or a family member may need long-term care in the future, Medicaid planning with a qualified elder law attorney can protect assets while ensuring eligibility. Ohio has a five-year “look-back” period for asset transfers, which means planning ahead is essential. Several elder law firms specialize in Medicaid planning, and your area Bar Association can provide referrals. Don’t wait until you’re in a crisis to explore your options—the earlier you plan, the more options you have.

• • •

The bottom line: Ohio’s Medicaid system is complicated, but it provides vital services that can dramatically improve quality of life for Ohio seniors. Whether you’re applying for the first time, renewing your coverage, or exploring waiver programs to stay in your home, help is available. Don’t try to figure it out alone.

Need help with Medicaid? Start with Pro Seniors at 1-800-488-6070. You can also contact your Area Agency on Aging. A list of Ohio AAA’s is available in any of our Ohio Older Adults Resource Guides at http://www.seniorimpact.com/view-our-guides. And share this article with a family that might need this information.